By Rob C

TLDR: Here we go again. Wall Street has once more re-engineered the mechanics of the financial system to ensure that the house always wins. In a breathtaking display of structural favoritism, SpaceX was waved through Nasdaq’s front door on a regulatory technicality. The very same five mega-banks that pocketed $646 million to underwrite its $75 billion IPO immediately turned around and recommended their clients to buy the stock—while independent voices were entirely shut out of the room. Predictably, despite a near-unanimous chorus of buy ratings, the stock still fell 12% in a week and is down 36% from its peak. This isn’t a glitch or a failure of the free market; it is Wall Street’s oldest, most reliable sleight of hand, freshly deregulated and back in business — and it’s the same trick that, forty years ago, took away your grandparents’ guaranteed pension and handed you a slot machine instead, with instructions to figure it out yourself.

Good morning, everyone. This is a bit of a follow-up to my article “The SpaceX IPO: A Pump and Dump Scam Aimed at Your IRA”. In that article, I wrote how that Wall St. coming-out party was like a fairytale wrapped in a gold-plated turd. This matters because many of us were invested in this POS company without our consent. Read on to learn how, once again, Wall St. and Trump are still screwing American workers.

The Fast-Track Fix

If you still retain a quaint, textbook belief that our financial markets operate on fair competition and an even playing field, the recent market debut of SpaceX should officially cure you of that delusion. What we witnessed wasn’t the invisible hand of the market at work; it was the visible hand of regulatory capture rewriting the rulebook in real time.

To get the massive $75 billion SpaceX initial public offering into the hands of institutional investors as quickly as possible, Nasdaq leadership simply decided to alter its own foundational listing criteria. Under normal, long-standing market guardrails, a newly public company is required to demonstrate at least three months of stable trading history and maintain a strict minimum public float before it can even be considered for inclusion in the prestigious Nasdaq 100 index.

But when the company hitting the block is owned by the world’s richest man and political mega-donor, the rules apparently become highly elastic. SpaceX didn’t just join the Nasdaq 100 — it got escorted in. Nasdaq completely discarded the three-month requirement, lowering the barrier to a mere 15 days of trading history while totally waiving the standard minimum float obligations. Think about what that actually means. The Nasdaq 100 isn’t just a scoreboard. It’s a list that triggers automatic, mechanical buying from every index fund and ETF benchmarked to it — collectively representing more than $800 billion in assets. Getting on that list means billions of dollars flow into your stock, whether or not a single human being decides your company was worth the money.

To frame this in sports terms: the referee didn’t just miss a bad call; the referee moved the goalposts before the whistle even blew, and everyone in the stadium was supposed to pretend that was normal. The entire apparatus was fast-tracked to manufacture instant liquidity for corporate insiders, ensuring the public index would absorb the stock before anyone had time to actually read the financial disclosures.

When Banks Grade Their Own Homework

Once the regulatory pathway was cleared, the high-finance cartel moved in to execute the core text of the grift. This is where we look at the absolute absurdity of an industry designed to grade its own homework.

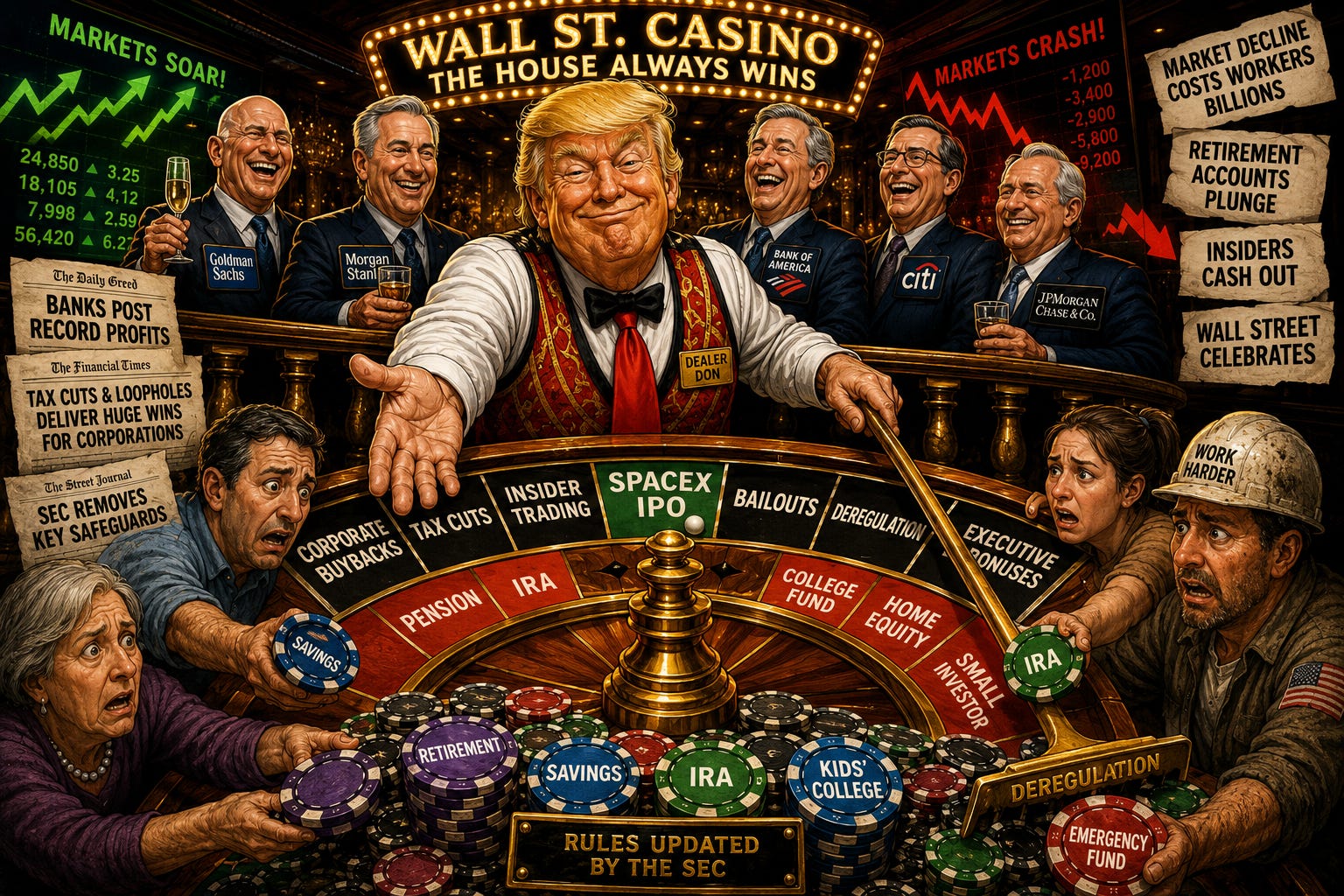

Now for the part that should make you actually angry. Five banks led the underwriting syndicate on SpaceX’s IPO: Goldman Sachs, Morgan Stanley, Bank of America, Citigroup, and JPMorgan. Goldman landed the coveted “lead left” spot — the name printed top corner of the prospectus, the bank effectively running the book. These exact five banking behemoths were paid an estimated $646 million in underwriting fees to bring SpaceX to the public market. They were explicitly hired by the company to market the stock, inflate the valuation, and ensure the IPO was a roaring success for the issuer.

And what did the internal research divisions of those exact same five banks do the moment the stock went live? They put on their supposedly objective “analyst” hats, looked at the company they had just been paid $646 million to hype, and issued glowing, breathless recommendations to their private wealth clients.

The data highlights a hilarious, unvarnished conflict of interest: 100% of the bank-affiliated analysts issued a definitive “Buy” rating on the stock. Meanwhile, among independent analysts who had absolutely zero financial ties to the underwriting deal, that “Buy” consensus dropped to a far more skeptical 65%. In fact, across the entire global field of financial research, there was only one solitary, brave “Sell” rating issued—and it came from an independent research firm with completely zero banking ties to Wall Street. He was also the only one who wasn’t, functionally, grading his own employer’s homework.

The sheer farce of this “objective research” is perfectly exposed by the wild divergence between the lead banks. Goldman put a $205 target on the stock. Morgan Stanley — a bank that helped underwrite the exact same offering, using the exact same prospectus, looking at the exact same numbers — said $300. That’s not a rounding error. That gap implies roughly a trillion dollars of disagreement between two firms that both got paid to make the deal happen. Raymond James, not even one of the lead underwriters, went further still: an $800 target implying a $10.5 trillion valuation, bigger than the entire stock markets of the UK, France, and Germany combined. When your “objective research” produces numbers with a trillion-dollar margin of error, it proves that modern Wall Street equity research is not financial science; it is glorified marketing copy disguised as analytical insight, designed to pump a stock until insiders can exit their positions.

But even a completely rigged game has its limits. Despite the coordinated wall of institutional “Buy” recommendations and the altered Nasdaq listing rules, the underlying financial reality could not be suppressed. Immediately following the fast-tracked index inclusion, the stock plummeted by 12% in a matter of days, bringing its total collapse to a staggering 36% down from its post-IPO peak. Even the combined marketing might of the five largest banks on Earth couldn’t keep the price from cratering under its own inflated weight.

The Rule They Killed to Make This Legal

If you are wondering how this blatant conflict of interest is completely legal, the answer lies in a quiet, calculated regulatory execution that took place just seven months ago.

Back in 2003, in the immediate, ash-covered wake of the catastrophic Enron and WorldCom collapses, the Securities and Exchange Commission (SEC) was forced to implement the Global Research Analyst Settlement. During the Enron disaster, the public discovered that 16 out of 17 Wall Street analysts were aggressively maintaining “Buy” or “Hold” ratings on Enron just two months before the company vanished into absolute bankruptcy, because their banks were desperate to secure lucrative investment banking fees.

To stop this corruption, the 2003 rule erected a mandatory legal firewall that strictly separated a bank’s analytical research department from its investment underwriting division. Analysts could no longer be paid based on the banking deals they helped close, and investment bankers were legally barred from influencing research reports.

But memory is short in Washington, and corporate lobbying power is eternal. Seven months ago, under the guise of “reducing compliance friction” and “modernizing capital formation,” the SEC quietly terminated the 2003 rule.

The warning signs were completely ignored. Former SEC Chairman Arthur Levitt took to the pages of The Wall Street Journal with a desperate, clarion warning titled “The SEC May Make Wall Street Analysts Corrupt Again”. Levitt outlined the exact predatory mechanism we are seeing play out today: if an analyst dares to rate a powerful corporate client as a “Sell,” that client will immediately retaliate by freezing the analyst’s bank out of the next multi-million-dollar IPO underwriting fee.

The Retaliation Mechanism:

Analyst Issues “Sell” Rating -> Corporate Client Gets Angry -> Bank Stripped of Next IPO Contract -> Ratings Drift Permanently Toward “Buy”

Consequently, the entire field of financial research naturally drifts right back into becoming a cheerleader squad for corporate clients. The firewall has been entirely dismantled, the wolves have been invited back into the henhouse, and the predictable result is the systemic fleecing of the investing public.

Who Actually Eats the Loss

This brings us to the final, most infuriating question of Our Broken Systems: when a rigged asset like SpaceX drops 36% from its peak, who actually absorbs the financial destruction?

It isn’t Goldman Sachs or JPMorgan. They already wired their $646 million in guaranteed underwriting fees straight into their vault before the stock ever started trading. It isn’t the corporate insiders or the billionaire executives who utilized the fast-tracked Nasdaq inclusion to liquidate their private equity into cold, hard cash.

The losses are eaten entirely by you. Because Nasdaq altered its rules to shove this volatile asset straight into the Nasdaq 100 index, the stock was automatically forced into every major passive index fund, mutual fund, and retirement account in the United States. If you have a 401(k), a pension, or a target-date retirement fund, your money was automatically used to buy this overvalued stock at its absolute peak to provide a profitable exit ramp for Wall Street’s favorite clients.

This is the ultimate evolution of modern corporate state capture. Generations ago, working-class Americans had access to defined-benefit pensions—secure, corporate-guaranteed retirements managed with strict fiduciary responsibility. Wall Street spent forty years systematically dismantling those pensions, replacing them with the 401(k) system. They took away your financial security and handed you a digital casino slot machine instead, forcing you to gamble your survival in a market where they control the software, own the regulators, alter the rules, and ensure that no matter how bad the crash is, the house always, inevitably, wins.

Wall Street isn’t occasionally unfair. It is a rigged game by design, and your retirement account is a mandatory bet.

F*CK ICE. RELEASE ALL THE FILES!

Please like, share, and subscribe — because the house doesn’t need your permission to keep cheating, but it would sure appreciate your applause.

Follow my work: Substack: democracy4sale.substack.com

Web: democracy4sale.com / Facebook.com/Democracy4sale1

Robert Cain is the author of “Democracy for Sale: How Corporate Greed Is Corrupting Democracy and Endangering the Planet.” Available at Amazon, Barnes & Noble, and independent booksellers everywhere.